I have not been tracking more recent changes in Irish banking sector aggregate balance sheets for quite some time now. However, preparing for a brief presentation on Irish banking crisis earlier this week, I had to update some of my charts on the topic. Here is some catching up on these.

Take a look at Central Bank’s data on credit and deposits in Irish banking system. These figures incorporate declines in both due to sales of loan books by Irish banks, so step-changes down on credit lines reflect primarily these considerations. As superficial as the numbers become (in this case, the aggregate numbers no longer fully reflect the true quantum of debt held against Irish households and companies), there are some positive trends in the figures.

- Over the 3 months through August 2015 Irish households have reduced the level of outstanding debt by some 7.1% compared to the same 3mo period in 2014. Total level of household debt now stands at the average of December 2004-January 2005. This is a massive reduction in debt burden, achieved by a combination of repayments, defaults and sales of loans to non-banking entities (e.g. vulture funds). However, loans for house purchases have declined by a more moderate 4.5% over 3mo through August 2015 compared to the same period in 2014. This brings current pile of house mortgages outstanding to the average level of February-March 2005. Which is impressive, but, once again factoring in the fact that quite a bit of these reductions was down to defaults and sales of loans, the overall organic deleveraging has been much slower than the chart above indicates. Over the last 3 months (though August 2015), total volume of household debt declined, driven down by deleveraging in mortgages debt and ‘other debt’ against a modest increase in consumer credit. It is interesting to note that over the last 12 months (based on 3mo average), volume of ‘other loans’ has dropped by a massive 38%, suggesting that this category of credit is now also subject to superficial debt reductions, for example originating from insolvencies and bankruptcies. For the record, there are at least three highly questionable reductions in recorded household debt on record: November-December 2010 drop of EUR7.5 billion, September-October 2011 drop of EUR17.2 billion, and May-June 2014 decline of EUR4.1 billion. This suggests that the official accounts of household deleveraging may be overstating actual degree of deleveraging by upwards of EUR28 billion which could bring our debt levels back to September-October 2011 and signify little material reduction in total debt over recent years.

- Over the 3 months through August 2015, loans outstanding to the Non-financial corporations in Ireland fell 19.4% compared to the same period average in 2014. Most of this decline was driven by the 19.5% drop in loans, with debt securities outstanding declining by only 5.7%. This marks 12th consecutive month of m/m declines in credit outstanding to the corporate sector. Current level of corporate credit brings us back to the levels last seen in 3Q 2003. Just as with households there are at least 3 episodes of significant declines in credit volumes since the start of the Global Financial Crisis, although the path for corporate loans has been more smooth overall than for household debt. This suggests that banks have prioritised resolving corporate arrears over household arrears, as consistent with 2011 PCAR strategy that also prioritised corporate loans problems.

Total credit outstanding to the real economy (excluding Government and financial intermediaries) has fallen 12% y/y in the three months through August 2015. The official register now stands at EUR145.3 billion, a level comparable to the average for June-July 2004.The truly miraculous thing is that, given these levels of deleveraging, there is no indication of severe demand pressures or significant willingness to supply new credit.

As shown in the chart below, Irish banking sector overall has been enjoying steadily improving loans to deposits ratios.

Over the July-August, household loans to deposit ratios dropped to 99% - dipping below 100% for the first time since the Central Bank records began in January 2003. Loans to deposit ratio for non-financial corporates declined to 120% also the lowest on record. However, this indicator is of doubtful value to assessing the overall health of the financial sector in Ireland. To see this, consider the following two facts: household loans/deposit ratios have been below pre-crisis lows since October 2011, while corporate loans/deposits ratios have been below pre-crisis lows since July 2014. Reaching these objectives took some creative accounting (as noted above in relation to loan book sales), but reaching them also delivered practically no impetus for new credit creation. In other words, deleveraging to-date has had no apparent significant effect on banks willingness to lend or companies and households willingness to borrow.

By standards set in PCAR 2011, Irish banks have been largely ‘repaired’ some months ago. By standards set in PCAR 2011, Irish banks are yet to start their ‘participation in the economy’.

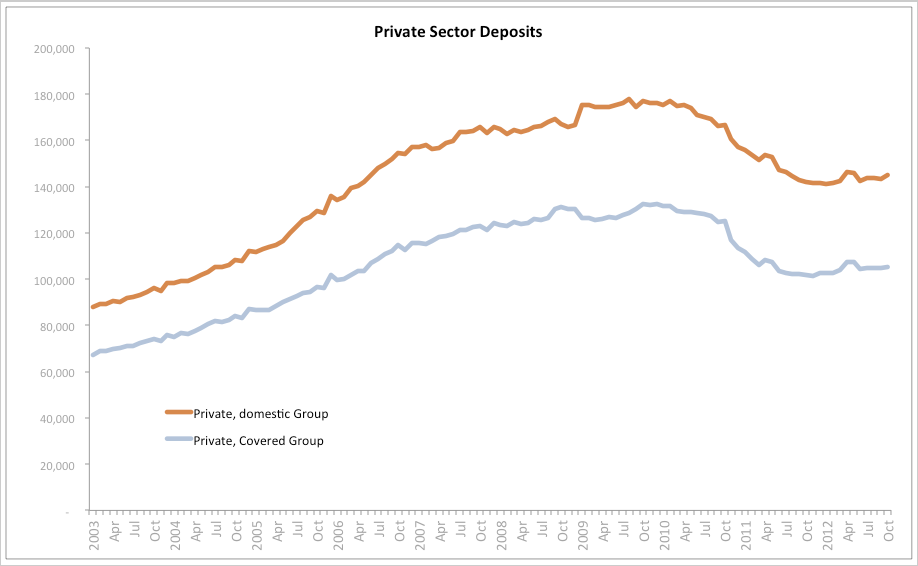

Meanwhile, take a look at the last chart:

As the above clearly shows, Irish banking system is nothing, but a glorified Credit Union, with credit outstanding ratio for household relative to corporates at a whooping 177%. This, again, highlights the simple fact that during this crisis, banks prioritised deleveraging of corporate debt and lagged in deleveraging household debt. Irish economic debt burden, thus, has shifted decisively against households.

Someone (you and me - aka, households) will have to pay for the loans write downs granted to companies over the years. And the banks are betting the house (our houses) on us being able to shoulder that burden.